Blog > How Much Home Can I Afford? A Step by Step Guide to Buying Smart Without Overstretching Your Budget

How Much Home Can I Afford? A Step by Step Guide to Buying Smart Without Overstretching Your Budget

by

🏡 Top FAQs: How Much House Can I Afford?

-

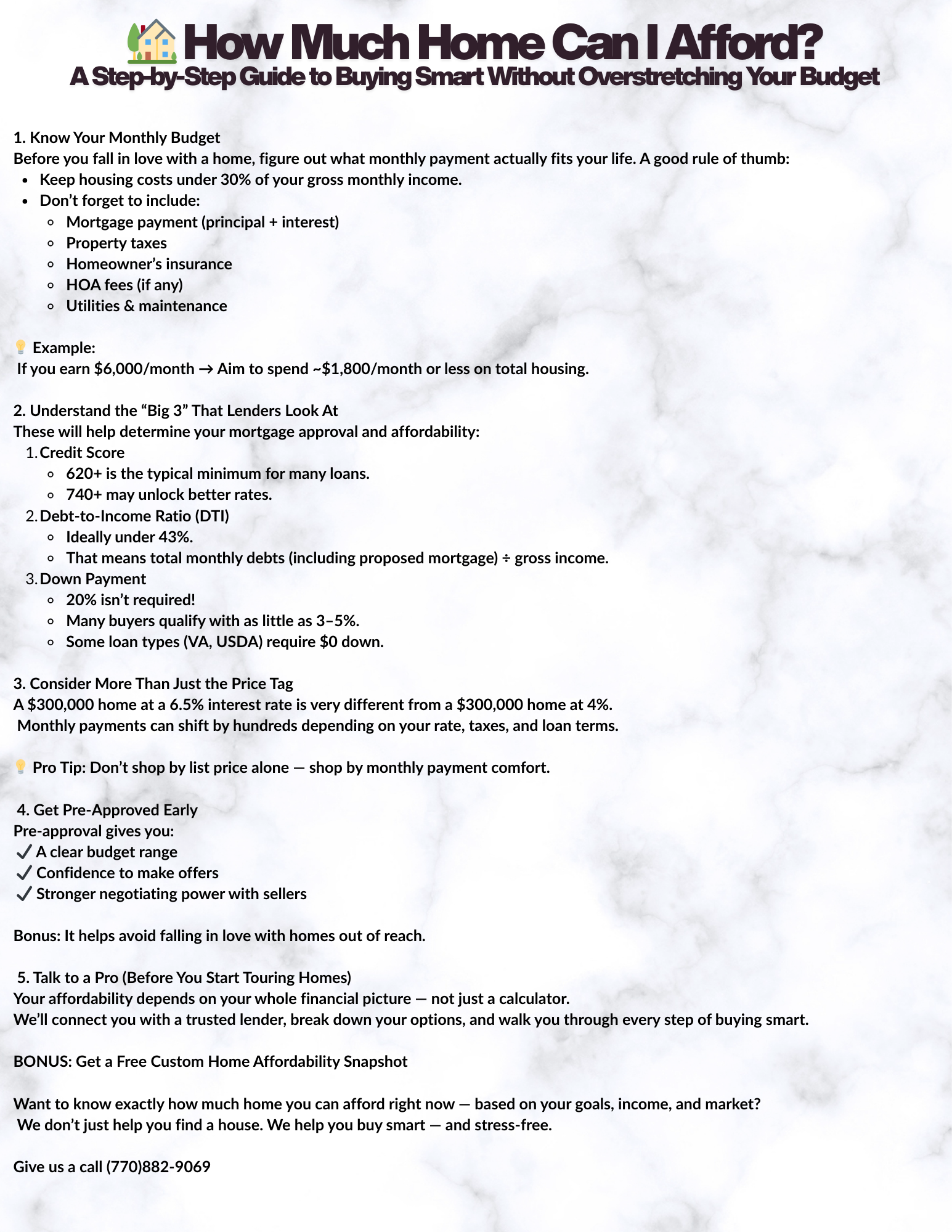

1. How do lenders calculate how much house I can afford?

Lenders use your debt-to-income (DTI) ratio, credit score, income, and savings to determine your loan eligibility. A typical rule is keeping your housing costs under 28–31% of your gross monthly income. The lower your debt and the higher your credit score, the more you may qualify for.

2. What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a quick estimate based on self-reported info.

Pre-approval is more in-depth—lenders verify your income, credit, and assets. Pre-approval carries more weight when making an offer, and gives you a clearer idea of your true buying power.

3. How much should I budget for monthly mortgage payments?

Your monthly mortgage includes principal, interest, property taxes, and homeowners insurance (often called PITI). Depending on the area, you may also have HOA fees or mortgage insurance. A lender can help break down these numbers based on your price range and down payment.

4. How much should I put down—and how does it affect what I can afford?

A larger down payment reduces your loan amount and may eliminate private mortgage insurance (PMI). But many buyers qualify with as little as 3–5% down, and some programs offer 0% down. The more you put down, the more flexibility you may have with your budget and monthly payments.

5. What hidden costs should I factor in besides the mortgage?

Beyond your mortgage, consider closing costs (2–5% of the home price), maintenance, utilities, and furniture or updates. Owning a home means budgeting for both expected and unexpected expenses—so it’s smart to leave room in your budget.